Guide to Uninsured Motorist Coverage Requirements in South Carolina for 2026

Driving in South Carolina comes with significant risks. Between 2013 and 2023, the state saw a staggering 34 percent increase in traffic fatalities. While state law requires all drivers to carry liability insurance, not everyone follows the rules. This gap in compliance leaves responsible drivers vulnerable to major financial losses after a crash. Uninsured motorist (UM) coverage is your first line of defense, a mandatory protection designed to shield you when the at-fault driver has no insurance. This guide will break down South Carolina’s legal requirements, clarify the protections your policy offers, and explain the critical steps to take if you are involved in an accident with an uninsured driver.

Understanding South Carolina’s Mandatory Insurance Laws

The “25/50/25” Minimum Liability Rule

South Carolina law mandates that every registered vehicle must be covered by a liability insurance policy. This policy must meet the minimum “25/50/25” limits, which means it covers: $25,000 for bodily injury or death to one person in an accident, $50,000 for total bodily injury or death to all people in a single accident, and $25,000 for property damage in a single accident. While this is the legal minimum, the high cost of modern vehicles and medical care means these limits are often exhausted quickly in a serious crash. In 2023, traffic crashes in the state resulted in a shocking $30.9 billion in societal harm, underscoring how quickly costs can escalate beyond minimum coverage.

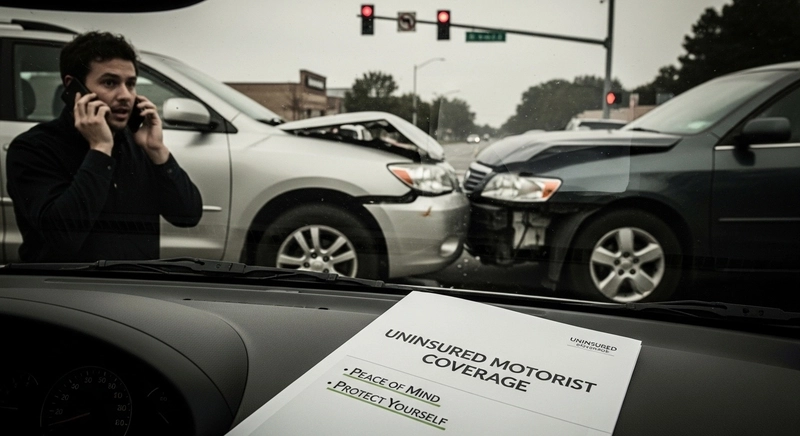

Uninsured Motorist (UM) Coverage: A Required Protection

In addition to liability coverage, South Carolina requires drivers to carry Uninsured Motorist (UM) coverage with the same minimum 25/50/25 limits. This crucial coverage steps in to pay for your injuries and damages if you are hit by a driver who has no insurance at all or by a hit-and-run driver who cannot be identified. The state’s requirement reflects the reality of the roads, where law-abiding drivers need a safety net to protect them from the negligence of others. Given that there were over 15,392 reported DUI incidents in South Carolina in 2023 alone, the risk of encountering an irresponsible driver is substantial and makes UM coverage a vital component of your policy.

Uninsured (UM) vs. Underinsured (UIM) Coverage: What’s the Difference?

Many drivers are confused by the difference between uninsured and underinsured motorist coverage. While they sound similar, they protect you in distinct scenarios. UM coverage is mandatory, while Underinsured Motorist (UIM) coverage is an optional but highly recommended addition to your policy. Understanding both is key to ensuring you are fully protected from the financial consequences of a car accident in SC. This distinction is critical for navigating the complexities of SC car insurance requirements and protecting your assets after a collision.

Key Distinctions Explained

| Feature | Uninsured Motorist (UM) Coverage | Underinsured Motorist (UIM) Coverage |

| Purpose | Protects you from at-fault drivers with no insurance or hit-and-run drivers. | Protects you from at-fault drivers with not enough insurance to cover your damages. |

| When it Applies | The at-fault party is confirmed to have no active liability policy. | Your medical bills and other damages exceed the at-fault driver’s liability policy limits. |

| Legal Status in SC | Mandatory for all drivers. | Optional, but strongly recommended. |

| Example Scenario | You are rear-ended, and the other driver fled the scene or provides expired insurance information. | You suffer $100,000 in medical bills, but the at-fault driver only has the minimum $25,000 bodily injury liability limit. |

How to Use Your UM Coverage After Being Hit by an Uninsured Driver

Being in an accident is stressful, and discovering the other driver is uninsured only adds to the complexity. However, this is precisely why you have UM coverage. Following the right steps after an accident with an uninsured driver in SC is essential to ensure you can access the benefits you’ve paid for. Properly documenting the event and your damages forms the foundation of a successful claim. This preparation is your best tool for holding the responsible parties accountable, even when the at-fault driver lacks insurance.

Immediate Actions to Take at the Scene

Your priority is safety and evidence collection. Doing this can have a meaningful effect on the final decision on your claim.

- Call 911: Report the accident immediately. A police report is crucial for any insurance claim, especially a UM claim, as it officially documents the incident and the other driver’s lack of insurance.

- Get Medical Attention: Even if you feel fine, get a medical evaluation. Adrenaline can hide injuries at first, with symptoms showing up later. This establishes a medical record that ties your injuries to the accident.

- Gather Evidence: If you are able, take photos of the vehicles, the accident scene, your injuries, and the other driver’s license plate. Get contact information from any witnesses.

- Do Not Negotiate: Avoid making any deals or accepting cash from the at-fault driver at the scene.

Navigating the UM Claim Process

Filing a UM claim means you will be dealing directly with your own insurance company. While you might expect them to be on your side, their goal is often to minimize their payout. The process can become adversarial, and proving the extent of your damages requires careful documentation and negotiation. If you face challenges or feel the settlement offer is unfair, consulting with an experienced South Carolina Car Accident Lawyer can be essential to protect your rights and pursue the full compensation you deserve.

Key Steps for Filing Your Claim:

A systematic approach to filing a UM claim in SC can prevent costly errors and delays. Follow these steps to build a strong case with your insurer.

Notify Your Insurer: Report the accident to your insurance company as soon as possible. Clearly state that the other driver was uninsured.

Provide All Documentation: Submit a copy of the police report, photos, witness statements, and any other evidence you collected.

Track Your Expenses: Keep detailed records of all medical bills, prescription costs, lost wages from time off work, and vehicle repair estimates.

Be Thorough and Honest: Cooperate with your insurer’s investigation, but be careful not to downplay your injuries or speculate on facts you are unsure about.

Understand Your Policy: Review the UM section of your insurance policy to understand your coverage limits and any specific requirements or exclusions.

Why Minimum Coverage May Not Be Enough in 2026

The dangers on South Carolina’s roads are increasing. A 2023 study identified South Carolina as the No. 3 state for distracted driving, while DUI-related incidents remain a serious problem, with advocates pushing for change after a recent fatal crash in Columbia. In 2023 alone, traffic crashes in the state resulted in a staggering $30.9 billion in societal harm, including medical costs, lost productivity, and property damage. With rising healthcare costs and the high price of vehicle repairs, the state’s minimum 25/50/25 coverage is often insufficient to cover the aftermath of a serious collision. A single hospital stay can easily exceed the $25,000 bodily injury limit. Opting for higher UM/UIM limits and considering policy features like “stacking” can provide a much stronger financial safety net for you and your family.

Secure Your Peace of Mind on the Road

Uninsured motorist coverage isn’t just another line item on your insurance bill; it’s a critical financial shield in a state with significant driving risks. By understanding your policy, knowing the difference between UM and UIM coverage, and being prepared to act after a crash, you can protect yourself from the irresponsible acts of others. Review your auto insurance policy today to confirm your coverage limits are adequate for the realities of driving in South Carolina. Ensuring you are prepared long before an accident even happens is the best way to maintain financial security on the road.